2 Fifths of FA

The Coalition’s fuel reserves announcement, costed against DCCEEW’s own data

Angus Taylor’s pre-budget commitment to lift Australia’s Minimum Stockholding Obligation from 30 days to 60 days arrived on 28 April 2026 with $800 million attached and a one-billion-litre storage promise. Costed against the Department of Climate Change, Energy, the Environment and Water’s own published data, the policy funds approximately one fifth of the storage required to deliver its own stated target. The target itself sits one third short of the IEA standard. Australia remains the only IEA member country that does not meet the 90-day net oil import obligation, and has not done so since 2012.

The policy lifts Australia from 30 days of consumption cover to 60 days. The OECD comparator average sits closer to 150 days. Sixty days is two fifths of where serious economies operate. The headline number on the announcement, benchmarked against DCCEEW’s own data, is two fifths of FA!

The OECD test

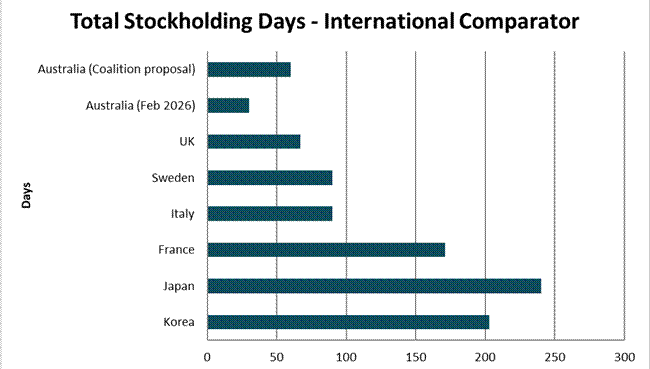

The international comparator data published in the Page Research Centre’s March 2026 paper, All at Sea: Fuel, War, and Australia’s Achilles’ Heel, sets out international stockholding regimes by country. Industry mandated reserves plus government-owned stocks, expressed in days of consumption. Korea holds 203 days. Japan holds 240 days. France holds 171 days. Italy and Sweden each hold 90 days. The United Kingdom holds 67 days, sitting on 57 percent domestic crude production. Australia holds 30 days, with no government-owned stocks at all.

The Coalition’s 60-day target lands closer to the United Kingdom than to any of the major OECD comparators. The United Kingdom holds that position with the buffer of its own North Sea oilfields. Australia would hold the same buffer with under 20 percent domestic crude production and no government reserve. The Coalition is proposing to match the European country with the most generous indigenous resource base while operating from the most depleted indigenous resource base in the OECD.

Total stockholding days held by country. Sources: Page Research Centre (March 2026), DCCEEW Australian Petroleum Statistics (Feb 2026 release).

The 41-day decline

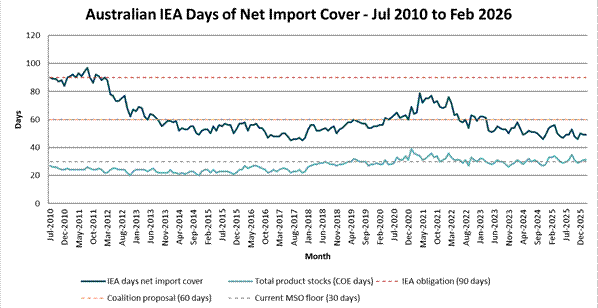

DCCEEW publishes a monthly time series of Australia’s IEA days of net import cover in the Australian Petroleum Statistics. The series begins in July 2010, when Australia held 90 days. The most recent value, February 2026, is 49 days. Australia has lost 41 days of cover over fifteen years.

The Coalition proposal would restore approximately 11 of those 41 days. The $800 million capital commitment is therefore a partial recovery to a position Australia held in early 2017, while the strategic context has deteriorated considerably since then. The remaining 30-day gap to the IEA obligation, and the 90-day gap to a serious OECD posture, is left untouched.

Source: DCCEEW Australian Petroleum Statistics, Feb 2026 release. Reference lines indicate the 90-day IEA obligation, the 60-day Coalition proposal, and the 30-day current MSO floor.

The arithmetic of the announcement

Australian total petroleum product sales for the twelve months ending February 2026 reached 62.8 gigalitres. Daily consumption averages 172 megalitres. Sixty days of cover at that consumption rate requires approximately 10.3 gigalitres of held stock.

Current Minimum Stockholding Obligation total held volumes, published by DCCEEW for the December 2025 quarter, sit at 5.3 gigalitres across diesel, gasoline, and kerosene. The increment required to deliver 60 days at current consumption is therefore approximately 5.0 gigalitres of additional held stock.

The Coalition has funded 1.0 gigalitre. The funding gap is 80 percent. The 1 gigalitre commitment delivers approximately 5.8 days of additional cover at current consumption. To meet the 90-day IEA obligation, the increment required above current MSO held would be approximately 10.2 gigalitres, or roughly ten times the volume the Coalition has funded.

The capital cost per litre of installed storage in the Coalition announcement runs at $0.80. That figure is consistent with above-ground refined product tank retrofit at existing common-user terminals such as Vopak East Arm in Darwin, Vopak Botany in Sydney, or the Coogee/Vopak cluster at Kwinana. It runs well above the $0.15-per-litre figure the Page Research Centre estimates for greenfield underground crude storage, where 12-month national cover at one million barrels per day consumption would cost approximately $5 billion in capital and $2 billion per year to maintain.

Storage capacity is not stockholding

A subtler problem sits underneath the funding gap. Funding 1 gigalitre of additional storage capacity does not cause 1 gigalitre of additional stock to be held. Storage is an asset. Stock is working capital.

Australian fuel importers run just-in-time replenishment because working capital is more expensive than the alternative cost of supply disruption under normal operating conditions. Tanks installed at common-user terminals generate hosting fees through long-term lease arrangements. Stock held inside those tanks ties up working capital at the importer’s cost of capital, and earns nothing absent a price spike.

Mining companies, for example, generally replenish to maximum receivable parcel size and absorb the working capital cost as the price of supply security. Australian fuel importers operate on the inverse logic, drawing tanks down to operational minima before triggering the next vessel. That commercial logic is rational at the firm level and disastrous at the national level. A national stockholding policy that does not reverse the incentive structure does not deliver national stock.

The MSO is the regulatory instrument that compels stockholding. Storage capacity is the physical precondition. The Coalition policy funds the precondition without strengthening the instrument. New tanks installed at Vopak Botany do not generate national fuel security. Stock policy generates national fuel security, and the operating cost of that stock policy is the financing cost of working capital plus the capital value of the molecules.

At a current diesel landed price of approximately $1,100 per cubic metre, an additional 5 gigalitres of held stock represents roughly $5.5 billion of working capital tied up. Financed at importer cost of capital, the annual carrying cost alone runs $440 million to $660 million. The Coalition has costed the tankage and ignored the carry.

The MSO inflation

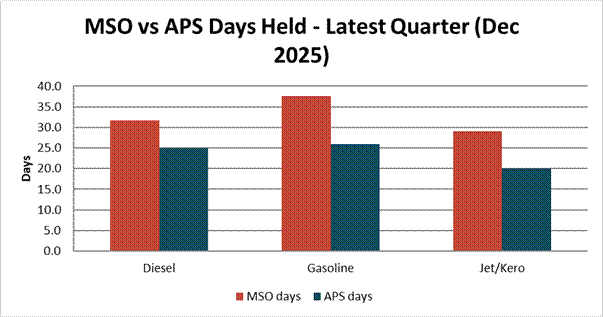

The Coalition’s 60-day target rests on an MSO measure that itself overstates the strategic position. DCCEEW’s MSO Statistics for the December 2025 quarter report 31.7 days of diesel held, 37.6 days of gasoline, and 29 days of kerosene.

The Australian Petroleum Statistics measures finished product on land in Australia and in domestic waters. APS reports for the same period: 25 days of diesel, 26 days of gasoline, 20 days of jet fuel. The MSO inclusions inflate the headline by 27 percent for diesel, 45 percent for gasoline, and 45 percent for jet fuel.

The MSO regime counts stock on water in the Australian Exclusive Economic Zone, including tankers steaming into Botany or Geelong with three days to go. The MSO regime also counts eligible crude oil and unfinished products at refineries. The DCCEEW glossary explicitly states that MSO statistics are not comparable with the APS finished product stocks.

The Energy Minister’s figures cited in the press coverage of the Coalition announcement, “44 days petrol, 33 days diesel, 30 days jet fuel,” are MSO-basis numbers. The APS-basis equivalents are 28, 25, and 20. The strategic position is roughly a quarter to a half worse than the political talking points imply.

Source: DCCEEW MSO Statistics (Dec qtr 2025) and Australian Petroleum Statistics (Feb 2026 release). The MSO regime bundles refinery feedstock and EEZ-on-water tankers with finished product on land. APS measures finished product on land only.

The production deficit Taylor is not fixing

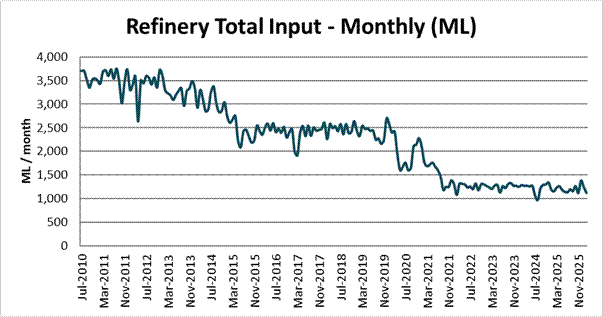

The deeper structural problem sits upstream of the storage debate. Australian refinery throughput, on DCCEEW’s own data, has collapsed. July 2010 monthly refinery input averaged 3,696 megalitres. February 2026 monthly input came in at 1,130 megalitres. A 69 percent decline in domestic refining throughput over fifteen years.

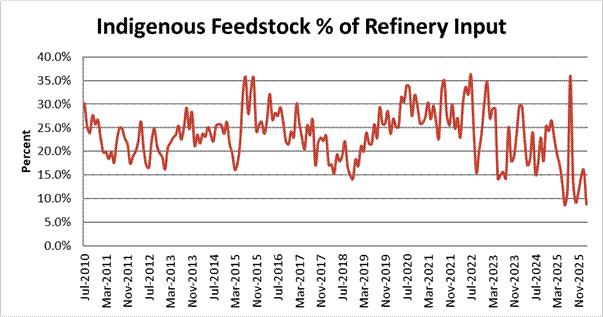

Indigenous feedstock as a share of refinery input has fallen from 30.1 percent in July 2010 to 8.8 percent in February 2026. The two surviving refineries, Lytton in Brisbane and Geelong in Victoria, run on imported crude for over 90 percent of their feedstock. Operational dependence on Singapore, Korea, Japan, and Middle East crude has deepened across every link in the supply chain.

Five Australian refineries have closed since 2012: Clyde in Sydney (Shell, 2012), Kurnell in Sydney (Caltex, 2014), Bulwer Island in Brisbane (BP, 2015), Altona in Melbourne (ExxonMobil, 2021), and Kwinana in Perth (BP, 2021). The two most recent closures, Altona and Kwinana, occurred during Taylor’s tenure as Energy Minister in the Morrison government. The Fuel Security Act 2021 was the response after the closures had already been announced, not before. The Coalition’s pledge to maintain Lytton and Geelong arrives after the structural damage is done.

Lytton operates at 112,000 barrels per day. Geelong operates at 120,000 barrels per day. Combined throughput against domestic demand of approximately 1,000,000 barrels per day delivers a maximum domestic refining coverage of 23 percent. Storage of refined product caps out at twelve months shelf life under good conditions and degrades faster in tropical climates and in fuels containing biodiesel blend stocks. Crude storage caps out at decades, and crude is only useful if there is refining capacity to convert it.

The strategic instrument is crude paired with refining. The Coalition has funded refined product tankage and pledged to preserve what remains of a 23 percent domestic refining base. The two pledges together do not constitute a fuel security policy. They constitute a slightly larger plank to march off.

Source: DCCEEW Australian Petroleum Statistics, Feb 2026 release. Total monthly refinery input has declined 69 percent over fifteen years.

Source: DCCEEW Australian Petroleum Statistics, Feb 2026 release. Indigenous feedstock has fallen from 30.1 percent of refinery input in July 2010 to 8.8 percent in February 2026.

The lag inside the announcement

The Coalition announcement landed on 28 April 2026, with the Strait of Hormuz constraint partially in effect and Asian refinery feedstock under pressure. The supply chain lag from crude lifting in the Middle East through refining in Korea, Japan, or Singapore to retail dispensing in Australia runs 60 to 90 days. Fuel pumped at Australian bowsers in late April was crude lifted before the conflict started.

The full effect of constrained Asian refinery throughput will appear in Australian terminal receipts in late May, with operational impact through June. The 60-day stockholding announcement is being made from inside the supply lag of an unfolding crisis, against a constraint that has not yet expressed itself in the supply data, on a target that does not meet the international standard, with funding for one fifth of the volume required to deliver the target.

The honest version

The policy as announced delivers two fifths of the OECD typical stockholding posture, funded at one fifth of the storage capacity required to meet its own stated target, against a target that itself sits one third short of the IEA obligation Australia has not met since 2012, in a national supply chain whose domestic refining base has collapsed by 69 percent over the same period.

The honest version of the announcement is that Australia is restoring less than a third of what was lost between 2010 and now, while remaining one third short of the IEA floor and at less than half of OECD typical cover. The structural production deficit is left unaddressed. The MSO inclusions inflate the residual headline. The funding mechanism subsidises tankage rather than compelling stockholding.

Taylor described the announcement as “a practical plan to make sure that never happens.” The data published by his own former department, on the day of the announcement, says the plan delivers two fifths of f#$@ a$$.

References

1. Department of Climate Change, Energy, the Environment and Water (DCCEEW), Australian Petroleum Statistics, February 2026 release. https://www.energy.gov.au/energy-data/australian-petroleum-statistics

2. DCCEEW, Fuel Minimum Stockholding Obligation Statistics, December quarter 2025 release. https://www.energy.gov.au/energy-data/australian-petroleum-statistics

3. Page Research Centre, “All at Sea: Fuel, War, and Australia’s Achilles’ Heel,” Policy Paper 02, March 2026.

4. Bureau of Infrastructure and Transport Research Economics (BITRE), Australian Infrastructure and Transport Statistics Yearbook 2025, Transport Energy and Environment chapter, December 2025. https://www.bitre.gov.au/publications/2025/australian-infrastructure-and-transport-statistics-yearbook-2025

5. Packham, B. and Chambers, G., “Fuel fracas: Coalition vows to double reserves to 60 days,” The Australian, 28 April 2026.

6. Fuel Security Act 2021 (Commonwealth of Australia). https://www.legislation.gov.au/C2021A00065/latest/text

7. International Energy Agency, Korea Oil Security Policy (2022); Japan Oil Security Policy (2022); Italy’s Oil Security Policy (2022).

https://www.iea.org/

8. ACIL Tasman, Petroleum Import Infrastructure in Australia, prepared for ACAPMA, February 2009.

9. DCCEEW, Australian Energy Statistics, Guide 2024. https://www.energy.gov.au/sites/default/files/2024-08/guide_to_the_australian_energy_statistics_2024.pdf

10. Future Fuels CRC, Underground Storage of Hydrogen, 2021. https://www.futurefuelscrc.com/wp-content/uploads/FutureFuelsCRC_UndergroundHydrogenStorage2021.pdf

11. Senate Standing Committees on Rural and Regional Affairs and Transport, Australia’s Transport Energy Resilience Report, Chapter 3, 2015. https://www.aph.gov.au/Parliamentary_Business/Committees/Senate/Rural_and_Regional_Affairs_and_Transport/Transport_energy_resilience/Report/c03

12. BP, Fact Sheet: A Guide to Storing Fuel. https://www.bp.com/content/dam/bp/country-sites/en_au/australia/home/products-services/fuels/opal-factsheet-storagehandling.pdf

Note on research support

Research support and data analysis assistance provided by Claude, an AI research assistant developed by Anthropic. The author retains full editorial responsibility for analytical judgements, framing, and conclusions.